As I often do, I'll start with a confession. Despite being a travel agent, and holding a handful of insurance licenses, I'm not someone who ever purchased travel insurance. It was an extra expense that seemed to go unused more often then not, so I passed every time.

In 2018, I went on an organized group trip to the Middle East. One of the requirements was proof of travel insurance. I purchased the plan they bundled with the trip, begrudgingly. On the second day of the trip, I woke up to severe pain in my lower left abdomen, and it got progressively worse. I had brought an over-the-counter pharmacy's worth of medicine with me, so I started taking what I thought might apply... Gas-X, ibuprofen... Nothing was helping. I ended up in a hospital with a kidney stone. I didn't know the language, I didn't know the medical system, and I didn't have a ton of cash to be spending on medical care.

The insurance company covered the bill, provided English support and I paid nothing out of pocket. They helped me navigate the system, and even covered my prescriptions which the hospital ordered. Ever since, I've been a convert. I don't travel without a travel insurance policy. Do I recommend them to all of my clients? Yes. Does every client need one? That's not for me to say. You know your situation better than anyone. What I can do is provide you with the information you need to make an informed decision.

If you'd like a cheat sheet of how to have a smooth claims process, take a look at (this article).

"Store Credit" or Cash?

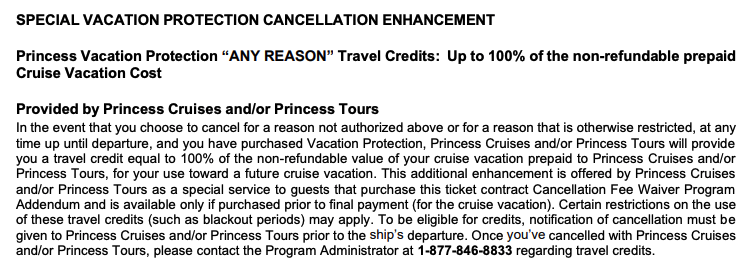

Many vacation providers--from airlines and hotels to cruise ships and resorts--provide some form of travel/vacation protection. This generally offers some amount of refund (usually in the form of a credit) in the event of a covered cancellation. They may not cover (or may not offer much coverage for) medical emergencies, lost baggage, etc. These credits may have expiration dates (i.e., must be used within 1 year of issuance).

The benefit here, is that often times, the credit is for more than you may find with a standalone travel insurance policy's 'cancel for any reason' coverage. In the above plan, you could get up to 100% of the non-refundable value of your cruise vacation. A standalone policy may only give a 50-75% cash refund.

Another consideration is what travel components they cover. If you book a hotel and flight separately from your cruise, will your cruise protection plan cover the flight and hotel? Maybe, maybe not... It may also limit the maximum amount of the reimbursement.

When you purchase a standalone travel insurance policy, you generally get a cash (i.e. ACH/EFT payment or check in the mail) reimbursement for covered expenses. You will tell the insurance company how much your trip cost, and that will generally set the limit of reimbursement. You maintain control of the policy.

Travel Insurance Glossary

While exact definitions will vary from plan to plan, I've included a list of frequently offered coverages in order to help you interpret what is being offered. If you're not sure, we're always happy to help. Feel free to reach out.

Before you go

Trip Cancellation: This protects your financial investment before you depart on your trip. If a covered event (think sudden illness, family emergency, natural disaster, etc.) were to occur and prevent you from taking your trip, this coverage would reimburse you for the non-refundable costs you've paid, such as airfare and cruise deposits.

Cancel For Any Reason (CFAR): This extends your cancellation coverage to include any reason not covered in the standard policy. If the week before your cruise you get a tarot reading, and the reader says you can't go on the cruise because you're going to meet your soulmate in your local coffeshop the day after the cruise leaves, and you decide to cancel your cruise--that's likely not a covered reason. If you have CFAR coverage, you would be reimbursed up to your plan's limit.

Covered cancellations can vary from plan to plan, so it's important to make sure that the plan you choose covers anything you're concerned might happen. Keep in mind that most covered cancellation reasons are 'unforeseeable'--meaning if they announce a blizzard is going to hit the day of your flight, and then you buy travel insurance, it likely will be excluded (since it's now a foreseeable incident).

While you are away

Trip Interruption: This coverage is for when your trip gets cut short for a covered reason. You may have to pay flight change fees or higher fares for last-minute flights. This coverage can reimburse for these extra expenses as well as the unused portion of your trip.

Trip Delay: This coverage is for things like being stuck at an airport or delayed for a period of time (the actual amount of time can vary by plan, but usually 5 or more hours) due to weather, mechanical issues, etc. This coverage can reimburse for extra expenses such as extra meals, toiletries, and even hotel rooms, depending on the situation.

Baggage & Personal Effects: This covers your physical belongings. If your airline loses your bags, if your bags are damaged, or if items are stolen while you are travelling, this can provide reimbursement for the value of your luggage and its contents.

Medical & Emergency Coverage

Travel Medical: This coverage comes as either 'primary' or 'secondary' coverage. Primary coverage is immediately available, and comes first before any other insurance you may have. Secondary coverage may require evidence that any other policies you may have would not cover the expense before it will kick in. Many US health plans provide little to no coverage outside the country, particularly on cruise ships. Travel medical coverage can cover doctor visits, urgent care, hospital stays, and prescriptions should you get sick or injured while travelling.

Emergency Evacuation: One of the most important coverages... This coverage isn't for the medical treatment itself, but instead can pay for the specialized transportation required to get you to the nearest appropriate medical facility. If you are in a remote area or at sea and need a medical flight back to a major hospital, this coverage can save you tens of thousands of dollars. Some plans also provide evacuation coverage in the event of a security situation.

It's all in the timing...

While some travel insurance policies and coverages can be purchased up to a day or more before your trip, other coverages have specific requirements as to when they need to be purchased. For most policies, the important date is the date you made the 'first deposit' towards your trip. While it may be tempting to fib, if you file a claim, you will need to show your receipts, which will include the purchase date.

First Deposit: For most policies, the 'first deposit' date will be the date you made the first purchase in relation to that trip. For instance, if you have a flight alert and find a great deal on flights from Boston to Paris, and book them--not knowing what else you'll plan, that becomes your 'first deposit' date. If you book the hotel 6 months later, the timer doesn't reset. It's all part of the same trip. For a cruise or resort vacation, the first deposit date may be the date you make your deposit, so long as you haven't purchased any other trip components previously.

Cancel For Any Reason: Many travel insurance companies require that you opt for this coverage within the first 10-21 days of the 'first deposit'. If you want this coverage, it's important to check the plan's requirements. As mentioned above, this coverage allows you to recover some of your non-refundable costs if you cancel for a reason not otherwise covered by the plan.

Pre-existing Conditions Waiver: Some travel insurance plans offer a waiver for pre-existing conditions. Generally this will also need to be purchased within 10-21 days of the 'first deposit'. Without this coverage, if you have asthma and on a shore excursion suffer an asthma attack, without this waiver, any necessary medical treatment may not be covered since it's a pre-existing condition. If you have existing conditions, it's important to check your plan's requirements.

Cancellation/Free Look Period: Most, if not all, travel insurance plans allow for a window of time (up to 10-15 days) for you to review the policy documents, and to cancel if you decide the coverage is not for you. Make sure to check your state-specific policy document to see what cancellation options you have.

Fringe benefits

Depending on the insurance carrier, there may be additional coverages provided by your plan, including concierge services, payments for changes to your cruise itinerary, payments for bad weather or theme park closures, etc. Some are included for no charge, and some are add-ons that can provide peace of mind (particularly if you're traveling in the off-season for lower rates).

The Bottom Line

You know your situation best. If you purchased refundable airfare and refundable hotels, have disposable income to spare, and are in excellent health, you may not opt for travel insurance. At the end of the day, insurance is there to cover non-refundable costs and unexpected additional expenses. If you have the means to handle them, you are self-insuring.

If you're saving for a vacation, and additional expenses are not something that your budget can handle, you should look at your options.

Since you made it this far, I'll share a pro-tip. Most travel insurance policies are quoted based on the total non-refundable amount of your trip. You may not know that initially, and further, many of your deposits may be refundable. You can often purchase a policy, inexpensively, with a $0 trip amount, locking in Cancel for Any Reason and applicable pre-existing conditions waivers. As you book more or as things approach the non-refundable window, you can increase the coverage.

If my team or I can be of any assistance, feel free to reach out.

Disclaimer: This post is meant to be a general summary designed to help you understand your coverage options at a glance. It does not reflect any one policy or provider. All claims are subject to the specific terms, conditions, and exclusions of your chosen policy. Benefit limits (the maximum amount the insurance will pay) vary by plan.

For a full list of what is and isn't covered, please refer to your Policy Certificate or Schedule of Benefits.